PEPPER Consumer - July 10th

More ways to say yes this winter |

|---|

|

|---|

|

|---|

The temperature’s dropping, and so are our rates.

We’ve reduced rates across key Consumer Motor Vehicle tiers, effective 13 July 2026 – giving you more flexibility on price and more opportunity to help customers get behind the wheel this winter. |

|---|

|

|---|

|

|---|

| What's new: Interest rate changes |

|---|

|

|---|

|

|---|

| Consumer Motor Vehicles

Tier A New/Demo - reduced by 0.40% Customer rate of 8.99% (can be dialled down to as low as 6.99%)

Used 0-5 - reduced by 0.24% Customer rate of 9.39% (can be dialled down to as low as 7.39%) |

|---|

|

|---|

|

|---|

| Consumer Motor Vehicles

Tier B New/Demo - reduced by 0.19% Customer rate of 10.29% (can be dialled down to as low as 8.29%)

Used 0-5 - reduced by 0.24% Customer rate of 10.49% (can be dialled down to as low as 8.49%) |

|---|

|

|---|

|

|---|

What you need to know:

The new applicable interest rate will apply to all: new applications created on or after 13 July 2026, pipeline applications submitted to settlements after 17 July 2026; and pipeline applications submitted before 17 July 2026 but require editing and re-submission (for any reason).

The existing approved interest rate will apply to all: Need the full breakdown? Head to Solana, click on the Pricing Plan tab for all applicable rates and download your cards there. |

|---|

|

|---|

|

|---|

MAPLE - July 8th

We’ve just sharpened our pricing with a 15bps reduction across all rates (excluding applicable loadings).

Our reduced headline rates are as follows:

- Passenger and Commercial Vehicles - from 8.15%*

- Heavy Commercial Vehicles (incl. Trailers) - from 8.40%*

- Wheeled Plant and Equipment - from 8.45%*

Now's the opportunity to stay competitive, convert faster and drive more settlements across your pipeline.

As we step into the new financial year, we’d also like to thank you for your support over the past 12 months. We value the partnerships we’ve built and look forward to continuing to grow and write more business together.

*Loadings may apply

? Looking to finance your next asset? Maple makes it easier with streamlined approvals, competitive pricing and a team that supports you at every step.

Pauline Montano

Contact Us

9am - 5pm, Mon to Fri (Sydney time)

FINANCE ONE - July 8th

Dear Valued Aggregation Partner,

We're writing to let you know that the latest HEM figures have now been updated and are effective from today.

Below is the updated HEM table for your reference.

At Finance One, we are committed to keeping our Aggregation partners informed of changes that may impact lending assessments. The updated HEM figures are as follows:

New HEM Figures (Effective Today)

Category | HEM |

Base Rate – Single | $1,845 |

Base Rate – Couple | $3,130 |

Base Rate – Adult Dependent | $1,285 |

Economy – Single | $1,370 |

Economy – Couple | $2,470 |

Economy – Adult Dependent | $1,100 |

Per Dependent | $350 |

METRO - July 7th

|

|

A new financial year deserves a fresh rate cut.

Metro Finance is decreasing rates by 15 basis points, effective for all new applications from Tuesday, 7 July 2026.

As a quick reminder, key documents including payout letters, statements and amortisation schedules can be accessed anytime via the MyMetro Self-Serve Portal.

|

|

A refresher on key limits: Wheeled Equipment

$250,000 for new-to-Metro clients, increasing to $300,000 with 12 months’ history. Passenger Cars & Light Commercials

$150,000 for new clients, up to $200,000 with 12 months’ history. Private Sale Upgrades / Replacements

Up to $250,000, with reduced private sale loading of 0.25%. Electric Trucks

Up to $250,000 for new customers, or $600,000 with full financials (max exposure $700,000).

1% rate discount on carded rate. All while maintaining the same streamlined submission and assessment process you know and trust?

|

|

A 1% rate discount applies for new electric vehicles, battery chargers, solar, and Electric Trucks, all under a 1% MetroEco rate discount.

For full details on eligibility and how to take advantage of this discount, check out our product booklet. |

|

|

|

| Download our rate sheet and get started today |

|

| Passenger Vehicle Streamlined Policy |

|

| Trucks, Trailers and Wheeled Equipment Streamlined Policy |

|

| Other Equipment Streamlined Policy |

|

| Replacement Streamlined Policy |

|

| Ballon/Residual Finance Streamlined Policy |

|

| Agri Product Streamlined Policy |

|

|

METRO - July 6th

|

|

We're excited to introduce a new enhancement that delivers a better vehicle inspection experience.You can now order vehicle inspections directly through the DoxAI platform, putting greater control and visibility at your fingertips. By enabling inspections to be arranged earlier in the process, this enhancement can help reduce approval and settlement delays while providing improved visibility and tracking of inspection reports. What You Need to Know When submitting an application to Metro: - Select "No" for 3rd Party Vehicle Inspection in the Quote Tab

|

|

- Upload the completed inspection report against the relevant special condition in the Docs & ID Tab

|

|

| For assistance with profile setup or ordering inspections, visit DoxAI | Help - Broker |

|

The Benefits at a Glance ✅ Order inspections earlier in the process ✅ Reduce potential approval and settlement delays ✅ Improved visibility and tracking of inspection reports ✅ A more streamlined experience from application to settlement This enhancement is optional, with the existing process remaining unchanged. It simply provides an additional way to order and manage vehicle inspections for introducers who prefer greater control, visibility and flexibility.

Another step towards a faster, more streamlined introducer experience.

As always, your Metro BDM and our Support Team are here to help if you have any questions or need support along the way. |

|

|

AMMF - July 1st

| Broker Administration Fee (BAF) Update – Effective 1 July 2026 | Broker partners, AMMF has undertaken a considered review of Broker feedback, recognising the structural cost pressures associated with the delivery of financial services. In response, and to better support Brokers in the current operating environment, we are updating the maximum Broker Administration Fee (BAF) available across the network, effective from 1 July 2026. Updated Maximum BAF Limits - Finance amount less than $50,000: $1,250 including GST (from $990 including GST)

- Finance amount greater than $50,000: $1,550 including GST (from $990 including GST)

These revised limits will apply to all new applications submitted from 1 July 2026 onward. Important Reminder Regarding Broker Administration Fees The Broker Administration Fee is a Broker-imposed charge and is not retained by AMMF. Brokers are responsible for determining when a BAF is applied and must ensure the fee is appropriate, reasonable, and clearly disclosed to customers. Following (Australian Securities and Investments Commission) ASIC’s recent review of the motor vehicle finance industry, Brokers are reminded to ensure the following: - Fees and charges are communicated transparently to customers

- Customers clearly understand the nature and purpose of any BAF applied

- Broker fees are not represented as lender charges

- Customer outcomes remain a primary consideration throughout the process

- All practices align with relevant regulatory and compliance requirements

ASIC has highlighted concerns around fee disclosure, third-party distribution arrangements, and oversight of customer outcomes. Brokers are encouraged to review current practices to ensure clear, accurate, and compliant communication of all finance-related costs. Actions Required Please ensure that: - Relevant Broker staff are informed of the new BAF limits

- Quoting tools, documentation, and internal processes are updated accordingly

- BAF disclosures remain clear, accurate, and compliant

For any questions, please contact your Business Development Manager or the Broker Support Team. Thank you for your continued partnership and support. |

|

AZORA - July 1st

We've made a couple of changes |

As of 1 July, our minimum tax invoice/refinance amount has increased to $10k (up from $8.5k) across all consumer car loan products - excluding fees. On the upside, Car Loan 4 now goes up to $75k inclusive of fees (previously $50k) - giving your clients more room to move on larger purchases. The updated Consumer Product Guide is attached below. Any questions, reach out to your BDM or Broker Support. |

ALEX BANK - July 1st

Start the new financial year strong

With the new financial year underway, we’re here to help you keep quality deals moving with simple finance solutions your clients can say yes to.

To support your July opportunities Alex.Bank continues our compelling offers across both unsecured personal loans and consumer asset finance.

For unsecured personal loans, we've seen strong uptake of our streamlined homeowner assessment using payslips only, giving eligible clients a fast and simple path to an unsecured personal loan with a great rate.

For consumer asset finance, we're continuing one of our most popular broker offers on secured car and caravan loans — backed by fast decisions, sharp pricing and support from a team that understands brokers. |

|

|

No establishment fee offer extended

Our $295 establishment fee waiver on secured car and caravan loans has been extended, with the establishment fee now waived for applications received up to 16 July 2026.

This is on top of our exclusive 0.5% p.a. discount for eligible homeowners and mortgage holders, helping reduce upfront costs while delivering even more value for quality asset-backed applications! |

|

|

Alex.Bank Secured Rate Table ~

|

~ A discount of 0.5% applies to applicants who currently own their home outright or are paying off a mortgage.

*Comparison rate based on $30,000 unsecured/secured loan amount and 5-year loan term. A quote/contract must be on file with total cost. #$295 Establishment fee (Secured) - waived for applications received up to 16 July 2026.

|

|

|

Alex.Bank Unsecured Rate Table^

|

^A discount of 0.5% applies to applicants who currently own their home outright or are paying off a mortgage. *Comparison rate based on $30,000 unsecured/secured loan amount and 5-year loan term.

|

|

|

See why more brokers choose Alex.Bank for personal lending and consumer asset finance. If you need to discuss scenarios, rate guidance, or want to workshop a deal, we're here to help.

|

|

|

|

SELFCO - July 1st

As we close out another financial year, we want to take a moment to sincerely thank you for your continued support and partnership.

Your support has been instrumental in driving strong outcomes for our clients, and we’re incredibly grateful to work alongside you. |

|

Due to strong demand, we’re excited to share that our EOFY campaign has been extended through to 30th September 2026 — now refreshed as our:

“Jump into Spring” campaign

From 7.49% across eligible deals.

Key criteria: - Primary assets: $100K – $300K

- ABN/GST: 4+ years (no continuity permitted)

- Applicant profile: Property owners

- Sales types: Dealer & private

- Asset age: Max 10 years at end of term

- Applications must Settle by 30th September 26

This is a great opportunity to keep the pipeline strong heading into the new season.

New rate card & product guide launched

To support you even further, we’ve introduced a refreshed Rate Card & Product Guide, giving you a clear overview of:

- Our full lending offering

- Updated credit parameters

- Deal submission requirements

|

New scenarios form — quicker answers, better outcomes

We’ve also launched a new scenarios form designed to streamline your enquiries. - Faster turnaround on deal scenarios

- Clearer upfront assessment

- Improved support from our team

Email completed forms to scenarios@selfco.com.au or send it back to me! |

|

Want to know more?

Join us for our upcoming Coffee with Credit webinar, featuring our Credit Manager, Aiden Forolo, alongside Jess Stevens, Senior Business Development Manager.

Together, they will cover our latest credit policies, walk through relevant case studies and real-world scenarios, and share insights on what to expect in FY27.

Coffee with Credit Webinar Date : Tuesday 28th July 2026 Time: 10:30 am AEST |

If you have any deals you’d like to workshop or questions on the new updates, please reach out — we’re here to help.

Thank you again for your partnership.

Let’s keep the momentum going. |

|

|

|

FIRSTMAC - JULY 1st

Updates on Balloon Payment |

|

|

Please be advised that effective Friday 3rd July 2026, balloons will no longer be available for new business Consumer Car loans at Firstmac. All existing customers will continue as per their contractual arrangements but this option will no longer be available for new business. Pipeline or in-flight applications submitted prior to Friday 3rd July 2026 have 60 days to settle with the balloon selected. Firstmac has NO rate loading on loan terms >5 years for Car or Caravan loans. |

|

|

MORRIS - June 30th

|

|

We wanted to take the opportunity to thank you for your support during FY26, which has been a record year of originations for us. We also wish to provide an update on several changes we have recently made across our product suite, pricing, fees, and documentation.

The changes are in effect on all new applications submitted from the 1st July 2026.

What's New?

Product Enhancements

> Introduction of two new product solutions, Streamline Plus and Primary Plus, designed to offer larger transactions, at reduced rates for property owners.

> Greater flexibility across a range of customer profiles, allowing us to assist more clients on a case-by-case basis.

> Expanded lending parameters to help brokers secure approvals on transactions that may sit outside traditional lender appetites.

> We now require 6 months bank statements on our Primary Product, enabling us to demonstrate servicing capacity more accurately and identify consistent cash flow trends over a longer period.

Rates & Fees

> Updates have been made across selected rate bands and fee structures to ensure we remain competitive while continuing to provide the service and flexibility you expect from us. Please refer to the attached product matrix and fee schedule for full details.

Contract Documentation

> We have refreshed our contract documentation to improve clarity, streamline execution, and enhance the customer experience.

> The updated documents are now required for all new applications submitted from 1st July 2026. We are able to assist with document preparation. Simply email settlements@morrisfinance.com.au with an invoice and the customers direct debit details and we can generate these for you.

Please find attached below our updated Product Matrix, Product Guides, Broker Guides and Settlement Contracts. |

|

These solutions provide additional flexibility for customers requiring higher loan amounts, specialized asset funding, or transactions that may not fit within conventional lending policies.

With 24-48 hour credit turnaround times we are in a strong position to start the financial year positively and support our broker network.

Our team is available to discuss these enhancements and help structure opportunities for your clients. If you have any current transactions that may benefit from these changes, please don't hesitate to reach out.

We look forward to helping you and your clients achieve even more success in the months ahead. |

|

|

BRANDED - June 30th

|

Hi

From 1 August 2026, we’re making a number of changes to our clawback, overs and commission structures for introducers. |

|

|

|

|

|

|

|

Clawback changesWe’re moving from a flat 100% clawback if a loan is terminated or paid in full within 12 months to a tiered structure: - Within 6 months: 100% clawback

- 7-12 months: 50% clawback

- After 12 months: No clawback*

This structure will apply to volume-based incentives, consumer and commercial clawbacks. Overs^- Commercial overs will reduce from 75% to 70% (excl. GST) across all tiers

- There is no change to overs on consumer loans.

Commission capsThe maximum commission payable per settled transaction is capped at the lesser of: - $20,000 (excl. GST); or

- 12% of the total amount financed

For the purposes of calculating commission, the maximum loan term recognised remains capped at 60 months. |

|

|

|

|

|

|

Our product guide will be updated with these changes and available in the QuickSell document library on 1 August 2026. If you have any questions about how clawbacks, commissions and overs are applied, or would like support when quoting or structuring deals, please contact your BDM. |

|

|

|

|

|

MONEY 3 - June 24th

| Good Afternoon,

We've made an update to the Money3 Product Guide, which will take effect from Wednesday 1st of July 2026.

These changes reflect our ongoing review and refinement of the Household Expenditure Measure (HEM).

Click to open the new Product Guide.

Please note: Any applications that were pre-approved prior to the 1st of July will continue to be assessed under the existing HEM figures.

As always, we appreciate your continued support of Money3.

|

|

|

|

AFFORDABLE CAR LOANS - June 22nd

METRO - June 17th

|

|

As part of our ongoing system improvements, we’ve released updates designed to support faster turnaround times and a smoother processing experience. These enhancements are intended to reduce back-and-forth and help streamline processing in the long run. Let’s get into it… |

|

New Address RequirementWe’ve introduced a new address field for properties entered in the Asset & Liability (A/L) section to improve data accuracy and consistency. How it works: - When adding a property, the address must now be entered into the new field

- The field uses Google’s address finder to help quickly locate and auto-fill details

- A manual entry option is also available if needed

|

|

New Resubmit ButtonWe’ve introduced a snazzy new “Resubmit” button that will appear in the bottom left of the screen whenever changes are made to an application. How it works: - When you begin making amendments, the Resubmit button will appear.

- Complete all required changes first, click save, then click Resubmit to ensure your updates are properly processed.

|

|

| For any questions or further clarification, your BDM is here to help. |

|

|

ANGLE - June 15th

Because we love supporting our brokers, we’re introducing a limited-time promotional eofy rate starting at 7.29% for top-tier, property-backed deals! Stay competitive and convert quality opportunities before 30 June with Angle. The 50bps discount will apply to: A++ & A+ property property-backed deals Deals submitted and settled between 15-30 June New applications from today

|

Check out an A++ scenario that qualifies for 7.29% Sole trader 8-year ABN Purchasing a truck via private sale Property in spouse’s name Up to 8% commission, with no additional rate loading

Check out an A+ scenario that qualifies for 7.79% Sole trader 4-year ABN Purchasing a 7-year-old motor vehicle via private sale Property in spouse’s name Up to 8% commission, with no additional rate loading

|

And even better - we’re here to get your deals settled. Angle Finance has no hard settlement cut-offs. Our team is ready to support same-day settlements right up to 30 June, helping you maximise every opportunity before EOFY. Key dates to keep in mind  Recommended submission timeframes: Recommended submission timeframes:

30 June settlements 30 June settlements

EOFY doesn’t need to be a scramble - we’re set up to help you get deals done right to the finish line. Talk to your BDM today. |

Log in to Broker Portal to submit a deal! For more info head to MyHub, your go-to for all things Angle. |

Cheers, The Angle Finance Team |

|

PLENTI - June 12th

Tier 2 now open to Thin File customers |

|

|

Effective today, we've expanded our appetite for Thin File borrowers, opening up more opportunities for those with limited credit history.

Thin File borrowers with a CCR Score of 750+ are now considered Tier 2, with rates starting from 11.35% p.a. |

|

|

|

| Thin files CCR Score ≥ 750 | Thin files CCR Score < 750 |

|---|

| Pricing | Tier 2 | Tier 3 | | Income Verification | Payslips | Bank Statements | | Max loan amount | $40,000 | $40,000 | | Vehicle Type | Car only | Car only | Note: - Self employed and sole traders will be required to provide bank statements.

- Balloons are not available for thin files.

|

|

|

|

|

Who is a Thin File Borrower? |

|

|

|

A non-homeowner with no active credit facilities reported in the last 24 months.

For a credit facility to be considered active, it must have been open for at least 4 months. Credit cards count (even if now closed), while BNPL and overdrafts do not.

This is another step in expanding our appetite for quality non-homeowner borrowers while making it faster and easier for brokers to do business with Plenti.

If you have any questions about these changes or would like to discuss a specific opportunity, please reach out to your dedicated BDM or RM. |

|

|

BRANDED - June 11th

|

Hi

As we approach the end of the financial year, a quick heads-up on upcomingfee changes. This is an opportunity to lock in our current pricing and close some EOFY deals.

Following our latest review, we’ll be updating some of our fees for new and resubmitted applications and loan documents generated from Wednesday, 1 July 2026.

|

|

|

|

|

|

|

Summary of changes for consumer and commercial loans | Fee Description | Fees | Establishment fee:

Charged for processing and approving a new loan application. Collected upfront and debited to the loan account with the first payment. It can also be financed into the agreement.

Consumer Plus or Consumer Sale by Instalments

Consumer Plus Private Sale or Consumer Private Sale

Chattel Mortgage, Commercial Plus or Finance Lease

Commercial Plus Private Sale or Commercial Private Sale |

$525

$625

$575

$675 | Account maintenance fee:

Payable on each repayment date.

for monthly, quarterly, half-yearly and yearly repayments

for fortnightly repayments

for weekly repayments |

$10.00 per month

$4.62 per fortnight

$2.31 per week | Dishonour fee:

Payable if we’re unable to withdraw money from a direct debit authority. | $20 per dishonour |

Summary of changes for consumer loans only

| Fee Description | Fees | Early termination administration fee

Charged to cover our administrative costs if a loan is repaid early and in full before its final payment date.

(See our Product Guide for details on the early termination fee, which is charged alongside the early termination administration fee in applicable cases.) | $70 |

|

|

|

|

|

|

Our updated Product Guide can be viewed below: |

|

|

|

|

|

|

If you publish Branded Financial Services information, please ensure your finance terms, conditions, and any promotional material are updated to reflect these changes. Thanks for your ongoing business and support. If you have any questions, please reach out to your Business Development Manager. |

|

|

|

|

|

METRO Consumer - June 10th

|

|

While we can't predict the future, we can help you spot servicing issues before they become surprises.

Our new Consumer Servicing Calculator is now live in the MyMetro Portal, our closest thing to a crystal ball for consumer loans.

With just a few clicks from the Home Page menu under Calculators, you can quickly and accurately assess your customer’s ability to service a proposed consumer loan, helping you structure with confidence from the outset.

|

|

You'll be able to: ✔ Instantly see monthly surplus or shortfall ✔ Identify servicing pressure points early ✔ Access automatically updated HEMS benchmarks ✔ Export results directly to PDF for your customer files

The right insights upfront can make all the difference when structuring a deal.

Your crystal ball may be in the MyMetro Portal, but our Consumer Team is here when you need us.

|

|

|

|

| We’d love your feedback! Please leave us a Google review here. |

|

Latest Rate SheetPlease see our new and improved Rate Sheet attached. |

|

|

WESTPAC - June 9th

| 1% p.a. rate discount now available for electric vehicles | We’re offering a 1% p.a. discounted rate on eligible electric vehicle (EV) transactions through Equipment Finance.

The discounted rate applies to Rate Specials listed in our weekly rate charts.

Based on the weekly rates chart issued 9 June 2026, the rates available this week are:- 6.75% p.a. for 24 - 48 month terms

- 6.85% p.a. for 60 month terms

Offer terms- Standard eligibility, credit criteria, fees, charges, terms and conditions apply.

- Rates may change weekly. Refer to the latest weekly rate chart for the full list of available rates.

- Rates are valid for 7 days, subject to settlement within that period.

- The offer is available for applications submitted on or before 31 August 2026.

This discount cannot be used in conjunction with any other offer or discount.

Eligibility |

| | | | Vehicle types | Cars, light commercial vehicles, trucks and buses | | Eligible EVs | Battery electric vehicles and plug-in hybrid vehicles | | Excluded EVs | Traditional hybrids (non plug-in) |

|

|

|

| Speak to your Business Development Manager or Relationship Executive for more information and refer to our weekly advertised broker rates. |

|

MONEYME AUTOPAY - June 5th

|

|

End of financial year is here! Please see our updates from May.

|

|

|

|

End of financial year is the perfect time to support your commercial clients looking to upgrade vehicles, equipment, or grow their business before 30 June.

We're making it even better by giving away two $100 Prezzee eGift Cards for every eligible Autopay Commercial Loan over $50,000 settled before 5pm AEST on 30 June 2026.*

$100 for you, $100 for your client.

This offer also applies to any commercial refinance deals, here's an email you can send to commercial customers looking to refinance and potentially lower their monthly repayments:

Hi [INSERT CLIENT NAME], The end of financial year is right around the corner. Now may be the perfect time to refinance your commercial vehicle loan. MONEYME Autopay makes refinance simple and is offering you a $100 gift card for June only if you settle a loan over $50,000 before 5pm on June 30th. If you want to take advantage of this offer, please reply to this email or give me a call. Kind regards, [INSERT YOUR NAME]

[MOBILE NUMBER] **Only available when you finance a commercial vehicle with MONEYME Autopay over $50,000 before 5pm on June 30th 2026. The $100 gift card is a Prezzee gift card which allows you to choose goods and services from over 100 retailers such as Amazon, Myer, Uber and many more. See the Prezzee website for full list of retailers. Specific terms and conditions apply to the use of eGift Cards, which can be viewed at the following address: https://www.prezzee.com.au/doc/terms-of-sale |

| Gift card info: Gift cards will be sent in July 2026 to you and your client. If you haven't received yours by 15 July, please contact the Broker Support Team. |

|

|

|

Rate updatesAs of 3 June 2026, we made a few updates across our broker products: No changes have been made to SocietyOne Personal Loans.

Download the updated guides: |

|

|

| Autopay private sale reminder | |

For private sale applications, please ensure the vehicle is not transferred into the customer's name before settlement. Transferring ownership before funding is complete will prevent us from proceeding with the application. |

|

|

|

LIBERTY - June 5th

Liberty is updating rates across our motor consumer and commercial product suites, effective Tuesday 9 June.

All current approved applications will be honoured, provided settlement takes place by Friday 12 June.

Updated Product guides are available in Lender Resources. For more information, please contact your Liberty BDM or contact our Introducer Hotline on 13 11 33.

FIRSTMAC - June 4th

End of Financial Year Special |

|

|

We are excited to announce that effective immediately, Firstmac has reduced all Secured Asset Fixed Rates for Car and Caravan loans by 0.20% for the month of June. This can further assist your customers with even lower monthly repayments, helping you secure more settlements for the End of Financial year. Don't miss out on this special with lower rates, improved origination fee structure, standard zero loading for loan terms >5 years and strong policy niches to help your clients into a new asset. Applications must be submitted before COB 30 June 2026 and must settle by 7 July 2026 to qualify for this end of financial year special. To view our updated car and caravan interest rates, click below. |

|

|

|

SELFCO - June 4th

At Selfco we’ve turned up the volume this EOFY with a targeted campaign, new product and enhancements to policy to help you write bigger deals, faster. |

|

EOFY Campaign (Limited Time)

- ABN/GST: 4+ years

- Profile: Property Owners

- Loan Size: $100K – $300K

- Supplier: Dealer or Private

- Assets: Primary

- Rates from: 7.49%

- Min Fleet size of 3 trucks for Transport and Logistics operator.

Apply by 30 June 2026 | Settle by 31 July 2026 |

|

New Product:

Professionals Motor Vehicle Product

- Up to $200K loan

- Rates from: 7.49%

- Profile:

- Property Owners max loan $200k

- Non-Property Owners max loan $150k with 20% deposit

- Terms up to 60 months

- Designed for established professionals

- Medico – Legal – Financial – Technical and Consulting

- Talk to your BDM for details of our detailed acceptable professionals list

Tradie Loan - 1 Day ABN - No GST

- Up to $75k for Property Owners

- Up to $50k for Non-Property Owners (with 20% deposit)

- Supplier: Dealer or Private

- Assets: Commercial vehicles and Commercial trailers/Trade based diggers

- Product Expanded - Now funding for commercial trailers + small diggers

- Strong fit with the $20K Instant Asset Write‑Off (IAWO) - creating an opportunity to fund multiple assets and maximise EOFY deductions

Talk to me today to find out more details about our Professionals Pack or Tradie Loan. |

|

Policy Enhancements Secondary Tier - Limit increased to $250K (prev $150K)

- No bank statements for Property Owners ≤ $150K

Tertiary Tier - Limit increased to $150K (prev $100K)

- No bank statements for Property Owners ≤ $100K

|

|

Thank you for partnering with Selfco, where we make finance simple and tailored to your clients’ needs, especially when it matters most. |

|

|

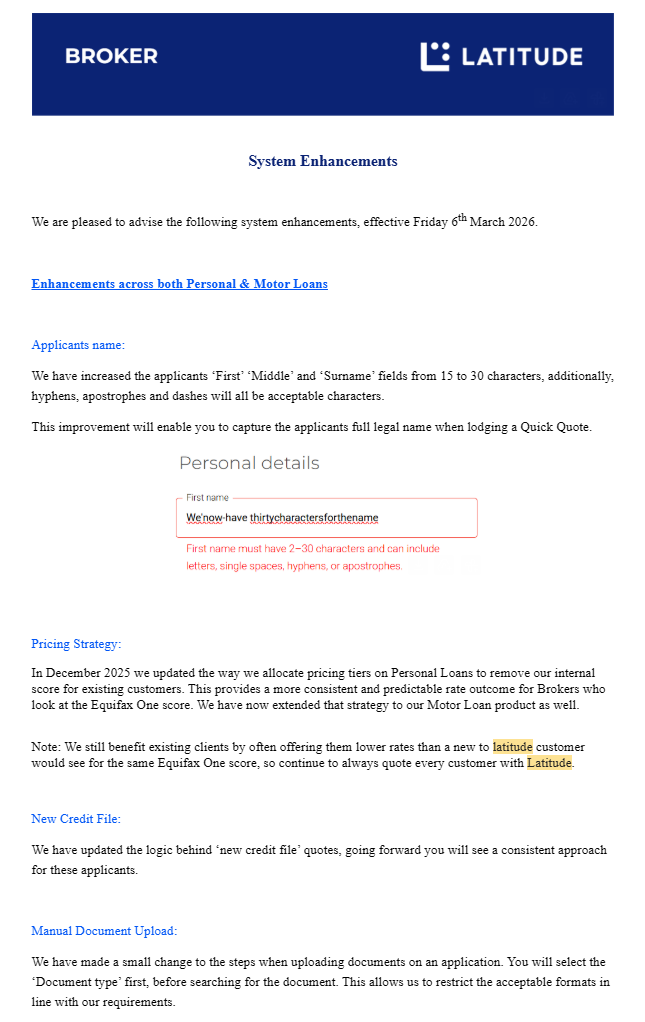

LATITUDE - June 3rd

|

Personal Loan & Motor Loan Interest Rate Changes |

Effective Thursday 4 June 2026, we are making changes to our Personal Loan and Motor Loan interest rates, including reductions to rates across a number of motor loan tiers. Our new pricing bands can be found in the table below and attached. Rates applicable for Latitude Personal Loan customers (Effective 4 June 2026) Rates eligible up to $200,000 | Pricing Tier | Variable Price range (Secured)^ | Variable Price range (Unsecured)^ | Fixed Price Range (Secured)^ | Fixed Price Range (Unsecured)^ | 1-5 | 9.99% - 15.99% | 9.99% - 16.99% | 9.99% - 15.99% | 9.99% - 16.99% | 6-10 | 16.99% - 20.99% | 17.99% - 21.99% | 16.99% - 19.99% | 17.99% - 20.99% | 11-15 | 21.99% - 25.99% | 22.99% - 26.99% | 21.99% - 25.99% | 22.99% - 26.99% | 16-20 | 26.99% - 28.39% | 27.99% - 29.39% | 26.99% - 28.39% | 27.99% - 29.39% | 21-23 | 28.39% | 29.39% | 28.39% | 29.39% |

Rates applicable for Latitude Motor Loan customers (Effective 4 June 2026) Rates eligible up to $200,000* | Mortgage Brokers | Finance Brokers | Pricing Tier | Fixed^ | Variable^ | Pricing Tier | Fixed Baseline Rate^ (at full 4.5% comm) | Variable Baseline Rate^ (at full 4.5% comm) | 1-5 | 7.99% - 11.99% | 7.99% - 11.99% | 1-5 | 8.99% - 12.99% | 8.99% - 12.99% | 6-10 | 12.49% - 14.49% | 12.49% - 13.99% | 6-10 | 13.49% - 14.99% | 13.49% - 14.99% | 11-15 | 14.49% - 16.99% | 14.49% - 16.99% | 11-15 | 15.49% - 17.99% | 15.49% - 17.99% | 16-20 | 17.99% - 21.99% | 17.99% - 23.99% | 16-20 | 18.99% - 22.99% | 18.99% - 24.99% | 21-23 | 21.99% - 21.99% | 24.49% - 26.99% | 21-23 | 22.99% - 22.99% | 25.49% - 27.99% |

Inflight applications – For quotes submitted prior to 4 June 2026 where the application is lodged on or after this date, the new pricing will apply. For applications approved prior to this date, the original pricing will apply. |

FINANCE ONE - June 3rd

We've cut rates, here's what's new!

While many lenders across the market are repricing upward, Finance One is doing the opposite.

From 1 June 2026, we're cutting base rates in our Commercial Asset Finance product. This gives you a sharper offer to take to your clients at exactly the moment they need it most. What's changing: - Platinum base rate REDUCED BY 1.50%

- Plus, Gold and Silver base rates REDUCED BY 0.50%

- Non-Homeowner loading on Plus REDUCED from 3.00% to 2.50%

|

^Current loading for Plus, Platinum, Gold & Silver across asset age and security type (primary/secondary) continue to apply. Rates and fees subject to standard credit assessment. |

Get your June pipeline ready. Talk to your BDM today. |

DYNAMONEY - June 3rd

We’ve recently amended our pricing and our updated Asset Finance Product Guide and Business Loans Product Guide. The changes can be viewed here. Please note that you will have 14 days to settle any existing approvals at the prior approved rate. Your Business Development Manager is here to support you, so please don’t hesitate to reach out if you’d like to discuss a scenario, workshop a deal, or simply have a chat. Thank you for your continued partnership. Kind regards,

The Dynamoney Team |

PLENTI- June 2nd

Rates reduced by up to 70bps |

|

|

We've just made a significant rate change to our Consumer Loan products.

Effective 1 June 2026, we're removing our rate loading on >5 year loan terms across both Consumer Auto and Personal Loan products. |

|

|

|

- 50bps lower rates on Consumer Auto Loans

- 70bps lower rates on Personal Loans

|

|

|

|

For customers looking for lower repayments spread over a longer term, the rates just got better.

This new pricing will apply to applications submitted on or after 1 June 2026. Please reach out to your dedicated BDM or RM if you have any questions or would like to discuss a scenario. |

|

|

Download the updated rate cards below to learn more: |

|

|

MONEYTECH - June 2nd

We've made an exciting enhancement to our Business Loan product that gives you and your clients access to more!

You asked, we answered. Live from today and in the Broker Portal, we're doubling our Business Loan facility limit from $500K to $1M. A significant enhancement that now gives you access to larger funding for your clients at a scale that actually matches what they need. |

|---|

|

|---|

|

|---|

Our Business Loans have gone bigger!

We're always sharpening our products to better support your clients and this time, we've kept it simple. Same policy, same streamlined bank statement assessment, same fast turnarounds. Just a bigger limit.

What this means for you: - Support stronger SMEs who need funding up to $1m

- Fast assessment, bank statements only - Lite doc

- Use the funds for a wide range of business activity including: wages, business acquisition, ATO debt, buyouts, refinance and general working capital

- Flexible security options, including second mortgage and caveat structures

- Bigger limits all under the one product making it easy for your clients

Check out the enhancements on our broker hub or via out product guide below. |

|---|

|

|---|

|

|---|

ALEX BANK - June 2nd

EOFY updates to help you finish the year strong

As we head into the final stretch of the financial year, we’ve made a few practical updates to help you keep deals moving and make the most of EOFY opportunities.

In this edition, you’ll find a new streamlined homeowner assessment option, making it faster and easier to lodge, alongside our extended no establishment fee offer on secured car and caravan loans – waived through to 30 June.

You’ll also find a process update to support faster progression, and some key pricing and calculator changes to be aware of when you next bank on Alex. |

|

|

Streamlined homeowner assessment

At Alex.Bank, we’ve just made it easier to place eligible homeowners and mortgage holders into an unsecured personal loan with a great rate.

Eligible clients can now be assessed using payslips only. That means no bank statements to request, upload or review.

This is a market-leading option built for clients who want speed and simplicity with no rate loading, meaning this option is available with interest rates from 7.49% p.a, and no application, ongoing, additional repayment or early termination fees.

Benefits for you - Faster lodgements with fewer documents to source.

- Less rework and fewer follow-ups for missing statements.

- Stronger homeowner proposition as a simple alternative to lenders who do not offer this or price it higher.

Benefits for your clients - Less hassle and fewer documents.

- More privacy with no day-to-day transaction sharing.

- Faster with a streamlined assessment process.

Eligibility criteria

To take advantage, borrowers must: - Be paying off a mortgage or own their home outright (mortgage holders verified via bureau credit report; homeowners are required to provide a rates notice to verify ownership).

- Have an Equifax Soft Score ≥ 750.

- Mortgage debt serviced for ≥ 12 months (if applicable).

- Have no arrears in the CCR.

- Not be a restricted borrower.

- Have an employment tenure in current role ≥ 6 months.

For homeowners who want an unsecured personal loan without the hassle of bank statements, Alex.Bank is the clear choice.

|

|

|

Want a quick walkthrough?

Join one of our upcoming webinars to see how the streamlined assessment works, and how to get the most out of it.

Tuesday 2 June 11.00am AEST - Register now

Try the payslip-only process today for eligible homeowners and mortgage holders.

|

|

|

Process update: Nominated Account Verification

To facilitate the streamlined homeowner assessment, we’ve introduced a new upload category: Nominated Account Verification, now available across all applications.

- For payslip-only deals, this is a mandatory document required for the loan to progress to assessment.

- For secured loans with payslips-only, this can be provided at submission or added later as an Approval Condition, if needed.

- If bank account details aren’t yet available, simply upload the payslip in this category at submission. Our team will recognise this and convert it to a condition where appropriate.

This update is designed to keep applications moving quickly with fewer hold-ups.

|

|

|

Extended no establishment fee offer

To keep your momentum going from now until the end of the financial year, we’re extending our no establishment fee offer on secured car and caravan loans, with the $295 establishment fee waived for applications received up to 30 June 2026!

|

|

|

CPI adjustment to Serviceability Calculator

We’ve updated our Serviceability Calculator to reflect the latest CPI changes, aligning Minimum Living Expense benchmarks to current cost-of-living data.

Please note as per current policy, benchmark figures are used as a general guide only. Benchmarks help provide a comparison point; however, they do not replace understanding a customer’s actual financial situation through bank statements, or broker conversations with customers for non-bank statement applications.

Reminder: Always access the calculator via the Broker Portal to ensure you are using the latest version. Any locally saved versions may be outdated.

|

|

|

Download our handy Product Guides

Want quick, simple resources to help your brokers sell more?

Download our Product Guides for Unsecured Personal Loans and Secured Personal Loans (Consumer Asset Finance). They’re built to make your conversations easier, outlining key features, eligibility, turnarounds, and how Alex.Bank helps you convert more clients, fast.

|

|

|

Alex.Bank Secured Rate Table ~

|

~ A discount of 0.5% applies to applicants who currently own their home outright or are paying off a mortgage.

*Comparison rate based on $30,000 unsecured/secured loan amount and 5-year loan term. A quote/contract must be on file with total cost. #$295 Establishment fee (Secured) - waived for applications received up to 30 June 2026.

|

|

|

Alex.Bank Unsecured Rate Table^

We’ve recently updated our Unsecured Personal Loan rates, with minor increases to two credit score bands across 1–5 year loan terms. Please review the latest pricing to ensure you have the most up-to-date rates when talking to your clients.

|

^A discount of 0.5% applies to applicants who currently own their home outright or are paying off a mortgage. *Comparison rate based on $30,000 unsecured/secured loan amount and 5-year loan term. |

|

|

|

|

|

|

WESTPAC - June 2nd

| Introducing SIMPLE+ Business Docs Only for Equipment Finance | We have recently refreshed SIMPLE+ (our streamlined submission pathway for business lending up to $5M) with the introduction of a simplified pathway for Equipment Finance lending from >$15k up to total lending $1.5M - known as SIMPLE+ Business Docs Only (BDO).

SIMPLE+ BDO allows for the use of an eligible customer’s BAS for servicing and removes the need for personal or accountant prepared financials. This makes the process faster and easier for customers and brokers, with quicker approvals, fewer documents, and a streamlined experience for everyone involved.

Eligibility for SIMPLE+ BDO follows similar criteria as SIMPLE+ with a few key differences: |

| | | | Lending limit | - Business lending up to $1.5M (for existing customers only)

| | Customer status | - BDO is available to existing Westpac Group Business customers only

| | Entity types | - SIMPLE+ BDO is available for Company borrower types ONLY.

- It excludes:

- Customers reporting under the GST Instalment Method

- Large PAYG withholders (classified by the ATO as withholding more than $1M)

- Sole Traders

- Individual ATF Trust

- Partnership with any individual partners

- Unincorporated Entities

| | Excluded industries | - SIMPLE+ BDO is not available for excluded industries within agriculture, aged care and nursing homes, childcare, food wholesalers and retailers, hospitals and pharmacies, property developers, religious organisations, franchises, not-for-profits, and travel agents.

|

Using SIMPLE+ BDO:- Confirm your customer meets the relevant SIMPLE+ and other eligibility criteria

- Complete a SIMPLE+ Application Form (Business Docs Only option) then, conduct a preliminary assessment using the BAS Calculator and the SIMPLE+ Serviceability Calculator

- Submit all required financial information and a Privacy Consent Form via DriveOnline

Please refer to our SIMPLE+ webpage which contains the below resources and further information.

SIMPLE+ Broker resourcesImportant: you must be an accredited Westpac Group broker to access the SIMPLE+ Serviceability Calculator and BAS Calculator. |

|

|

|

AMMF - May 29th

| QLD Broker BDM Appointed | Valued partners,

We are pleased to announce the appointment of James Dixon as our new QLD Business Development Manager. James brings extensive experience within the broker and asset finance industry, with a strong focus on supporting broker networks across the automotive and recreational vehicle sectors. He has a proven track record in building and strengthening broker relationships, delivering tailored finance solutions, and identifying growth opportunities in a highly competitive market. His background also includes significant experience in operational leadership and sales, where he has successfully led teams, enhanced performance, and delivered customer-centric outcomes across both wholesale and retail finance channels. James’ deep understanding of broker distribution and commitment to partnership-driven growth will be instrumental in supporting business in Queensland.

For all broker-related enquiries, please reach out to James:

M: 0439 457 853

E: james.dixon@ammf.com.au |

|

WESTPAC - May 25th

We have introduced several exciting DriveOnline enhancements effective immediately. |

|

| 1. Wet signature option for upfront affordability declaration - New to Bank DriveXpress/Medical policies | We heard your feedback and have acted. You can now choose for your customer to manually (wet) sign the upfront affordability document. The option to sign electronically remains available.

We have also removed the requirement to complete a second affordability form as part of the loan document pack. This removes duplication and helps speed up the origination process.

For a full walkthrough of this process, please refer to the training pack. |

|

| 2. Matrix eligibility expanded for Insurance Premium Funding (IPF) | Matrix eligibility for IPF has expanded. The allowable increase in the proposed premium has risen from 125% to 150% of the previous year’s premium, with all other eligibility criteria unchanged.

This makes it even easier to help your customers fund their insurance premiums and keep their cash for other important business expenses. |

|

| 3. eSign now available for Equipment Finance buyback and private sale applications | We’ve expanded eSign eligibility.- Direction to Pay (DTP) documents have been updated to support eSign.

- The DTP has been updated to clearly request the account holder name, rather than the bank account name, where applicable.

How does it work?- Buyback: the customer will receive both the DTP and loan documents in a single eSign package.

- Private sale: the customer will receive their loan documents in one package, while the DTP will be sent separately to the vendor to ensure customer documents remain confidential.

Please note that for both scenarios, you can still issue the DTP manually and obtain a wet signature if preferred. This option is now supported within DriveOnline. For a full walkthrough of this process, please refer to the attached training pack. |

|

| 4. Updates to the EF Client Identification Form (CIF) | Two minor updates have been made to the CIF:- Section L (broker/employee details) have been updated to include appropriate clauses to support the use of Smart Verify.

- A new section has been added to capture Foreign Tax Residency information for company as trustee structures. This information was previously captured via email and will now be collected directly in the form, removing the need for this additional step.

If you have any questions or need support with these changes, please reach out to your Business Development Manager or Relationship Executive. |

|

|

|

BANJO - May 22nd

Before rates.

Before repayments.

Before you even apply.

|

|

|

|

Your new first step for brokering deals with Banjo. |

Does your deal look like a winner? See if it’s got what it takes – in minutes! Without committing your clients and before racing too far down

the track. |

|

| |

|

You spoke, Banjo listened |

Our brokers asked for faster, easier ways to assess deal suitability before spending time on application forms. Enter Fast Fit! |

A tool built on real expertise |

Fast Fit reflects how our credit team thinks. All it takes is a few simple steps for an indicative answer on your deal compatibility with Banjo. Delivered in minutes. |

The warm-up before the sprint |

Fast Fit allows you to explore deal fit with no strings attached. Draw from the clarity and confidence of Fast Fit for better early-stage conversations and decisions. |

Start the race for the deal on the right foot |

|

|

|

AZORA - May 22nd

PLENTI COMMERCIAL - May 21st

COMMERCIAL LOANS WITH PLENTI |

Lower repayments or greater flexibility? |

|

|

We’ve been working on something big.

Plenti Commercial now offers two products for your commercial clients!

The new Plenti Advantage product sits alongside our existing commercial offering, now known as Plenti Flex.

We now have two clear loan structures for your customer, depending on whether they are driven by lower repayments or loan flexibility. |

|

|

|

Plenti Advantage:

For the Rate-Sensitive Borrower |

Ideal Client: Borrowers committed to the full term and focused on the sharpest pricing. Key Benefit: Lock in lower monthly repayments for long-term ownership. Payout Calculation: Net present value of all remaining repayments which haven’t yet fallen due, including any residual value or balloon payment, plus any fees and charges payable on termination. Broker Commission: No clawbacks in the event of early payout. |

|

| Plenti Flex:

For Flexibility and Control |

Ideal Client: Those who may upgrade, refinance, or pay out ahead of schedule. Key Benefit: Supports extra repayments and lower early payout costs. Payout Calculation: No early termination fee after the first 2 years on all loans. Broker Commission: Standard clawback terms apply, reflecting the loan's flexible structure. |

|

|

|

You can switch an application between Plenti Advantage and Plenti Flex at any time before settlement, giving you the flexibility to ensure you won’t have to start from scratch if a client changes their mind.** |

|

|

|

The Bottom Line for Brokers |

This dual-product structure gives you a clear competitive edge: Offer Plenti Advantage for a sharper, competitive rate when a client intends to see out the full term. Offer Plenti Flex when the possibility of an early asset upgrade, refinance, or payout is a key consideration for your client. |

|

|

|

To support the launch, we've also built a new Commercial Broker Guide based on the questions and scenarios our BDMs hear most.

Inside: Everything you need in one place—rate cards, policy guides, FAQs, and key contacts.

|

|

|

|

MOULA - May 21st

Moula have made the below changes to their product - updated product guide can be found in lender resources.

Key changes:

• New loans up to $500,000 for up to 5 years

• Minimum 12 months in business

• Asset-backed guarantor required for loans over $250,000

Please reach out to your Moula BDM if you have any questions.

METRO - May 20th

|

|

Our MetroEco Electric Truck offering is designed to make financing straightforward and commercially viable, with a 1% rate discount under the streamlined product you know and trust.

Access up to $250,000 under streamline for new customers or go further with full financials up to $600,000 per transaction, with a maximum exposure of $700,000 to support both new purchases and growing fleets.

Designed for brand-new electric trucks (3.5t GVM and above), the product follows Metro’s clear and consistent credit parameters.

As electric trucks continue to gain traction, MetroEco gives you a practical, competitive way to support clients looking to transition their fleets.

For full details, refer to the booklet here, or reach out to your BDM with any questions. |

|

|

|

| Download our rate sheet and get started today |

|

| Passenger Vehicle Streamlined Policy |

|

| Trucks, Trailers and Wheeled Equipment Streamlined Policy |

|

| Other Equipment Streamlined Policy |

|

| Replacement Streamlined Policy |

|

| Ballon/Residual Finance Streamlined Policy |

|

| Agri Product Streamlined Policy |

|

|

WESTPAC - May 19th

| We have changed our inspection requirements for trailers. | We are regularly looking to improve our policies and processes.

From today, Tuesday 19th May 2026, we have increased our inspection threshold for trailers only.

Moving forward, we will no longer require an inspection where the asset cost ≤$125,000 (previously ≤$75,000).

As a reminder, where you are funding an asset that doesrequire an inspection, our current pathways to complete this are by using one of the following:- Business Development Manager and/or Account Manager

- Westpac Group Accredited Broker and/or AAA member ≤$150,000

- RedBook RVA (virtual inspection) ≤$300,000

- RedBook Physical Inspections ≤$1,000,000

Your actions

For noting only. If you have any questions, please contact your Business Development Manager. |

|

|

|

FLEXICOMMERCIAL - May 18th

Through times of challenge over the years, flexi has proved we're more than fair weather friends, and the current economic conditions are no exception. Starting with a rate drop, here's how we're getting behind our brokers and their customers through thick and thin. |

|---|

|

|---|

|

|---|

RATES DROPPED ACROSS THE BOARD – LIMITED TIME!

Despite rising interest rates, we've taken the decision to DROP ours by 25bps across all standard primary, secondary and tertiary rates and flexipremium rates, effective as of 15 May – but they can't last forever.

It means the time to get your flexi applications in, is NOW. For full details of the rate drop, download our latest Rate Card below. |

|---|

|

|---|

|

|---|

OTHER WAYS FLEXI CAN HELP

In tough economic times, existing customers can be stretched on their commitments – and new customers can be hesitant to commit. flexi can help in both scenarios.

1. Existing customers feeling the crunch? Mid-term refinancing may be an option* – existing customers who are at least 12 months through their flexi asset finance contract may be eligible to refinance their contract over a longer term to reduce repayments and improve cash flow.

*Mid-term refinances are subject to normal flexicommercial credit policy.

2. New customers hesitant to commit? Where customers are hesitating due to inflation or cash flow worries, flexi can help with: - Old finance meets new – bundling an existing agreement into a new loan contract with additional equipment can allow the customers to both pay off the existing asset and purchase a new one, with the net result of reduced repayments.

- flexipremium Low Start Loans – for flexipremium facilities, we can offer repayments at 50% of the total for the first 3 months. This means less pressure on cash flow while the asset gets working, and allowing time for economic pressure to stabilise.

Download our fact sheets, then talk to your flexi BDM.

Inside, you'll find examples of how these solutions can assist cash flow and keep opportunity alive for businesses during these turbulent times. |

|---|

|

|---|

|

|---|

Any customers severely impacted by the current fuel crisis? Please reach out to your flexi BDM sooner rather than later. |

|---|

|

|---|

|

|---|

PLENTI - May 13th

CONSUMER AUTOMOTIVE LOANS |

Better pricing, higher loan limits |

|

|

Boarders and Living with Parents (LWP) borrowers applying for consumer automotive products have been traditionally harder to place with lenders, often defaulting to less competitive pricing, lower loan limits and more admin. |

|

|

|

With Plenti, that’s changed. |

|

|

|

Boarders and LWP borrowers with a CCR score ≥600 who are not a thin file can access: |

|

|

|

| Boarders and LWP now have access to Tier 2 pricing instead of Tier 3 |

|

|

|

| Higher borrowing capacity |

Up to $55K, subject to credit assessment |

|

|

|

| Simpler income verification |

Payslips accepted for PAYG applicants, reducing the need for bank statements (self-employed applicants still require bank statements) |

|

|

|

Turn your past 'no-gos' into opportunities. Revisit your boarder and living with parents deals and see whether we can help you get them a great deal. Your next deal might be closer than you think.

If you have any questions, please feel free to reach out to your dedicated BDM or RM.

|

|

|

|

MORRIS - May 13th

|

|

Following the recent RBA announcement and ongoing increases in the cost of funds, we will be implementing adjustments to some of our products.

These changes are necessary to ensure we can continue providing competitive and sustainable lending solutions to our broker network.

Linked below are the updated Morris Products, Product Matrix and Fee Schedule effective from today, Wednesday 13th May 2026.

Also included are copies of our current Broker Guide and Submission Cover Sheet for your reference.

We appreciate your understanding and continued support. Please reach out to your State Manager should you have any questions regarding the updated pricing.

|

|

|

MONEYME - May 12th

|

|

On Wednesday 13 May, MONEYME Personal Loans will introduce Energy Upgrade Loans, giving you a new way to support customers upgrading their homes, from solar and batteries to insulation, heating and cooling, and EV charging.

As more customers invest in energy-efficient homes, you can now offer rates up to 3.14% p.a. lower than standard MONEYME Personal Loans on eligible deals, when working with a NETCC-approved supplier. This offering is exclusive to the broker channel.

The process is the same as a MONEYME Personal Loan, just select ‘Energy Upgrade Loan’ as the loan reason and upload the NETCC supplier invoice in additional documents. Funds will then be paid directly to the supplier.

View the new rates and download the FAQs: Energy Upgrade Loans are available through MONEYME Personal Loans for homeowner customers (but not through SocietyOne Personal Loans). |

|

|

|

|

Need support? Our Broker Support Team is here to help on 1300 908 068.

Best regards,

The Broker Support Team |

|

|

BRANDED - May 12th

| Hi

We’re making changes to our interest rates, effective Friday 15 May 2026 (Effective Date).

You can find the full details in our updated product guide below: |

|

|

|

|

| | To ensure a smooth transition, we’ll honour the current rates for loans that meet all of the following criteria: - Approved by 5pm AEST Thursday 14 May 2026

- Settled by 5pm AEST on Friday 29 May 2026

- Not resubmitted for reapproval on or after the Effective Date.

Our updated commission calculator will be available in our document library from 15 May 2026. |

|

|

|

|

|

Expanded eligibility for our Ultra Prime rateFollowing feedback from introducers, we’ve lowered the Ultra Prime minimum credit score threshold from 990 to 960, which means more customers may now be eligible for this pricing tier. |

|

|

|

|

|

Need help workshopping a deal?Our dedicated support team is ready to workshop deals before submission. Contact Nick Lomliengbhol at workshop@brandedfinancial.com or call 1300 114 041, option 3 during business hours. Thank you for your continued support. If you have any questions about these changes, please contact your BDM. |

|

|

|

|

|

|

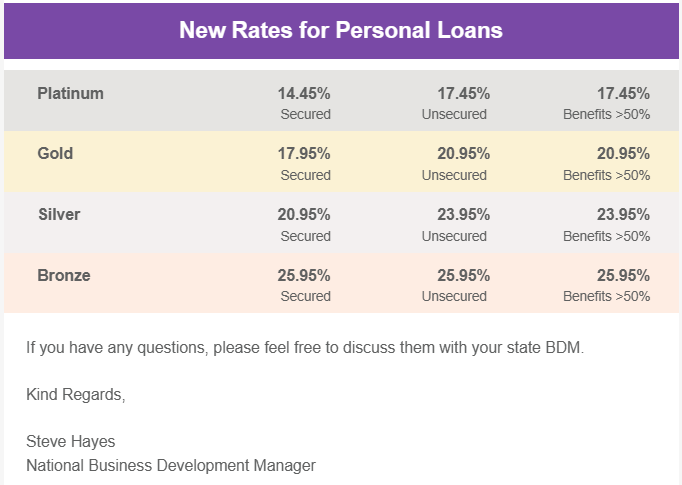

MONEY 3 - May 12th

| Good Morning,

We're writing to let you know that we have made a further adjustment to our Platinum tier rates. As with our previous communication, rising funding costs continue to place pressure on our pricing, and we have acted to reflect this as responsibly as we can. The changes to our Platinum rates will take effect on Friday 15th May 2026.

We have also provided a list of acceptable Visa's which you can download here.

The updated Platinum rates are outline below. All other tiers remain unchanged at this time. |

|

|

|

Asset Finance - M3 Asset Finance | Asset Finance - Micro Motor | Asset Finance - Benefits > 50% | Personal Loans - Secured PL | Personal Loans - Unsecured PL | Personal Loans - Benefits > 50% |

|

| | 14.95% | 14.95% | 17.95% | 14.95% | 17.95% | 17.95% |

|

|

|

| | Serviceability Calculator

We've also updated the repayment calculator to reflect these changes. You can access the updated calculator below. | | Download the Calculator |

|

|

|

FIRSTMAC - May 12th

Secured Asset Rate Change |

|

|

Following the RBA’s decision to increase the official cash rate, Firstmac will be increasing secured asset variable interest rates by 0.25% for all existing customers, effective Friday 15th May 2026. These changes will be reflected in P&I loan repayments from 27th June 2026. We have also reviewed our new business rates for variable, secured asset loans, effective 15th May 2026. Fixed rates will remain the same. To view all of Firstmac’s updated secured asset loan rates, please refer to the rate sheet linked below, effective 15th May 2026. |

All pipeline variable rate applications in progress will receive the 0.25% increase effective 15th May 2026. |

|

|

WISR - May 11th

BIG news - we’ve cut the BS (bank statements, that is) ?

We’ve expanded No Bank Statement assessments, anticipating that an excess of 80% of Secured Vehicle Loans will not require bank statements for assessment!

What you can expect | ✅ Quicker decisioning from submission to settlement | ✅ More seamless experience for you and your clients | ✅ Less admin, more momentum on every deal | | Start an SVL application |

|

| What else is new at Wisr? | We’re always working on making the lending process simpler and faster for brokers. Explore our latest updates below! | | Read more |

|

|

|

AZORA - May 8th

PEPPER - May 4th

We're updating our commercial pricing |

|---|

|

|---|

|

|---|

We're making some changes to our Asset Finance commercial pricing on 5 May 2026. |

|---|

|

|---|

|

|---|

What you need to know:

The new applicable interest rate will apply to all: - new applications created on or after 5 May 2026,

- pipeline applications not yet submitted to settlements by 9 May 2026; and

- pipeline applications submitted before 9 May 2026 but requires editing and re-submission (for any reason).

The existing approved interest rate will apply to all: - pipeline applications submitted to settlements before 10 May 2026.

Need the full breakdown? Head to Solana, click on the Pricing Plan tab for all applicable rates and download your cards there. |

|---|

|

|---|

|

|---|

AZORA - April 30th

Our 5.5% upfront broker commission promotion has been extended (again). That means you’ll earn 100% of the application fee plus up to 5.5% (incl. GST) of the loan size upfront with dial down options still available.

The increased upfront commission applies to Consumer Car Loans 1 and 2 for all new and existing applications settled by 30 June 2026.

Here's how it looks in action - rates from: |

7.79% - 3.5% upfront + up to $1,990 application fee |

8.79% - 4.5% upfront + up to $1,990 application fee |

9.79% - 5.5% upfront + up to $1,990 application fee |

Why Azora Car Loans 1 and 2? |

Rates as low as 7.79% with dial down Non-homeowners: renters & boarders - no loading Older assets: up to 20 years EOT - no loading Longer terms: up to 7 years - no loading High-mileage vehicle: up to 280,000km - no loading Mid-term and balloon refinance - no loading Private Sales - no loading Award winning flexibility

|

For any more questions, feel free to get in touch with your BDM.The Azora Team |

BRANDED - April 29th

|

Hi,

We’re pleased to introduce DoxAI digital invoices as part of our private sale process – designed to help you settle faster, reduce rework, and lower risk, while delivering a smoother experience for customers, at no cost to you. |

|

|

|

|

|

|

What’s ChangingDoxAI already supports a secure, end‑to‑end digital inspection for private sale vehicles. Sellers complete a guided inspection, submitting photos, vehicle documents, and ID, all of which are reviewed in real time and securely shared with Branded Financial Services.

This process now extends through to digital invoicing, removing the need for manual tax invoices and creating a faster, cleaner path from approval to settlement. |

|

|

|

|

|

|

The DoxAI Invoicing ProcessOnce the digital inspection is complete: - A private sale digital invoice can now be generated within the DoxAI portal

- Vehicle, seller, buyer, and bank details are pre‑populated from verified inspection data

- The invoice is electronically signed and securely stored

- Updated, compliant terms and conditions are applied consistently across transactions.

For more information, please refer to the DoxAI private sale invoice user guide, now available in our documents library. |

|

|

|

|

|

|

What This Means For You- Faster settlements

- Fewer errors and rework

- Lower risk of fraud

- Less admin for you and your team

- A better experience for your customers

- Faster decisioning and fewer post-approval queries.

|

|

|

|

|

|

If you have any questions, please contact your BDM. |

|

|

|

|

|

DYNAMONEY - April 25th

Given the current economic environment, we’ve made an adjustment to our Low Doc policy for asset finance. Effective immediately, Low Doc will be temporarily suspended for customers operating in the transport and construction sectors where: The asset is being purchased via private sale (excluding passenger cars and light commercial vehicles), and/or The customer is not asset-backed

We want to emphasise that we remain committed to supporting brokers and clients in these sectors. These deals can still be considered under our Easy Doc process, with 6 months’ bank statements provided via bank link. This approach allows us to continue supporting your clients while ensuring responsible lending in the current market conditions. If you have any questions or would like to discuss a scenario, please reach out to your BDM. Thank you for your continued partnership. Kind regards, The Dynamoney Team |

MONEYTECH - 24th April

Moneytech Business Support Program - 7.99% on sedans, utes, vans - now including EVs

As part of the Moneytech Business Support Program, we've sharpened our Equipment Finance special.

Electric vehicles have been officially introduced alongside sedans, utes and vans at our headline rate from just 7.99% p.a.

What this means for your clients

With fuel and operating costs still front of mind for many businesses, EVs are becoming an increasingly attractive option for businesses and fleets. Brokers can now offer EV finance with the same sharp pricing, simple process and fast turnaround your clients already expect on standard vehicles.

• Sedans, utes vans and now EVs

• Rates from a sharp 7.99% p.a

• Seamless application and approval process

• Accessible now via the Moneytech Broker Portal |

|---|

|

|---|

|

|---|

If you're not already accredited with Moneytech, this is a great time to start. Join our network today or head to our Broker Portal to submit deals. To learn more, reach out to your Moneytech BDM today! |

|---|

|

|---|

|

|---|

DYNAMONEY - 23rd April

We’ve recently amended our pricing and our updated Asset Finance Product Guide can be viewed here. Please note that you will have 14 days to settle any existing approvals at the prior approved rate. Your Business Development Manager is here to support you, so please don’t hesitate to reach out if you’d like to discuss a scenario, workshop a deal, or simply have a chat. Thank you for your continued partnership. Kind regards,

The Dynamoney Team |

FIRSTMAC - 21st April

Introducing Firstmac Caravan Loans |

|

|

We’re excited to announce that Firstmac has officially launched Caravan Loans, effective today! This new product is available to homeowners and covers both new and used caravans (up to 7 years old) – including private sales, with loans up to $150,000.

Loan terms and pricing match our current car loan offering, including no loading for 7 year loan terms. |

|

|

MONEYTECH - 17th April

Equipment Finance updates - Bigger deals, smarter processes, same sharp rates, backing businesses when they need it most

As part of the Moneytech Business Support Program, we're making a number of enhancements to our Equipment Finance offering, effective today, Friday 17 April.

They're designed to support larger deals, cleaner submissions, and a smoother broker experience for the businesses that need it most right now. Most importantly, we can now offer Equipment Finance limits of up to $2 million with financials, opening the door to larger, more sophisticated opportunities through our Broker Portal.

What's new

Rate Update - No rate increases to support your clients during this period

Higher limits, broader opportunity - EF limits increased up to $2m

- Applications for higher limits are now live and accepted via the Broker Portal

- Ideal for established trading businesses with supporting financials

Smarter policy requirements- EF purchases >$100k, bank statements required

- EF purchases <$100k, bank statements no longer required

- Sole trader and partnerships are no longer accepted

- No deposit and no credit references for non-property backed clients

These updates allow us to scale limits responsibly while maintaining strong credit outcomes, helping support long-term funding reliability for your clients.

Broker Portal and Tech upgrades To support these changes, we've rolled out key enhancements to our leading Broker Portal: - ID Matrix now integrated - streamlining AML/KYC Checks

- New bank statement upload functionality, making submissions faster and easier

- New quote calculator with embedded pricing matrix, enabling fast, accurate and downloadable quotes

- Less friction, fewer touchpoints and quicker deal progression

We're committed to backing brokers with clear policy, improved technology and the ability to support larger, quality deals. The above changes are effective from today, Friday 17th April and are part of our ongoing work to support both our brokers and their clients through our Business Support Program. |

|---|

|

|---|

|

|---|

If you're not already accredited with Moneytech, this is a great time to start. Join our network today or head to our Broker Portal to submit deals. If you have questions or want to discuss a scenario, your BDM is readyto help. We’re open for business and ready to support your next deal. |

|---|

|

|---|

|

|---|

FINANCE ONE - 14th April

PLENTI - 14th April

COMMERCIAL LOANS WITH PLENTI |

Larger assets. Greater opportunities. |

|

|

Trucks have landed at Plenti Commercial.

You can now finance trucks of any size - with no tonnage restrictions - giving you more opportunities to get deals over the line. |

|

|

| - Tier 1 businesses (3-year ABN, 2-year GST)

- Asset-backed customers with comparable credit

- Proven repayment history (existing or recently paid-out facility within 6 months, 12+ months conduct)

|

|

|

| - Loans up to $250,000

- Dealer purchases only

- No tonnage restrictions

- Desktop valuations accepted (completed by Plenti)

|

|

|

| - Prime movers, concrete agitators, food trucks

- Private sales or refinances

|

|

|

| - No early termination fees after 2 years

- Re-amortisation available

- 2–7 year loan terms

- Up to 35% balloon over a 5-year term (asset ≤10 years at loan end)

|

|

|

| - 25bps load for trucks over 12T

- Existing policy for trucks up to 12T remains unchanged, including private sales and refinances for Tier 2 and non-asset-backed customers (within current limits)

|

|

|

WISR - April 14th

From 15 April, we’re updating our rates across several products to reflect recent market movements.

We appreciate your understanding as we make these adjustments to stay responsive to the changing environment while continuing to offer competitive options for your clients, with rates from 6.14% (comparison rate 7.58%1).

In-flight applications will not be impacted, unless there are changes to the product type.

| | View rate card |  |

|

|

|

AZORA - April 10th

MONEY 3 - April

MAPLE - April 9th

Rates increased by 25 bps, effective 9th April.

PLENTI Consumer - April 9th

CONSUMER AUTOMOTIVE LOANS |

Your latest automotive loan

rate update is here |

|

|

Given the ongoing volatility in global markets and funding conditions, please be advised that we will be increasing our consumer automotive loan rates, with new headline rates starting from 9.39% p.a., effective Monday 13 April 2026.

The new rates will apply to all consumer automotive loan applications submitted from Monday 13 April 2026, and applications currently in the pipeline that have been submitted but not yet settled will retain existing rates until close of business, 20 April 2026.

Download the updated rate card below to learn more: |

|

|

If you have any questions about these changes or would like to discuss an opportunity, please reach out to your dedicated BDM or RM. |

|

|

|

ANGLE - April 2nd

Dear Angle Brokers, A quick update on what’s new at Angle - including an important rate change and how we’re continuing to support your deals: Rate update - see the latest rate card Your deals, backed by a bigger team More scenarios covered. More deals funded (EOFY incentive live)

|

Rate Update - check the latest rate card to see the updates. Our team will walk you through an exclusive breakdown of all changes at next National Webinar. Don’t miss it!

>> Thursday 16 April at 2:00 PM. |

We now have 3 new Business Development Executives (BDEs) managing their own portfolios - say hello to Grace, Luke, and Zac! Our priority? Supporting brokers like you with faster, easier finance. And there's more to come! Stay tuned for news about our Manager for the BDE team and new Heads of Distribution. Full team details here. |

Our BDMs have been out on the road delivering Bingo kits, check out some of the photos, what champs! Not into Bingo? No worries - did you know we’re actively backing a wide range of deals, from Start-Ups and Low Doc to Full Doc deals supported by strong financials? Take a look - you might be sitting on opportunities you didn’t realise we could support. |

METRO Consumer - April 1st

While the timing may suggest otherwise, unfortunately this isn’t an April Fools’ joke.